There are now an estimated 675 AD plants in the UK generating green gas of which the majority supply biogas to CHP’s that generate electricity for grid export and heat. A smaller number, circa 100, inject the green gas directly into the gas grid after removing CO2. Gas to grid is the most efficient application of biogas technology and the one that has attracted further Government support as it is a direct substitute for natural gas. Decarbonising the UK heat network is a key policy objective and a number of strategies are under consideration including biogas, heat pumps and hydrogen all of which present significant challenges. Whereas biogas (Anaerobic Digestion) is a well established global technology and a good substitute for natural gas it still requires subsidy support in order to attract long term investment capital.

The initial growth of the industry was driven through the introduction of long term tariff incentives which degressed as more plants were built. A key assumption of tariff support was that the costs of building plants would fall as the industry grew but this hasn’t really been the case. This is partly due to the nature of AD plants which typically consist of four separate components: a concrete slab, large digester tanks, a lot of pipework and a grid connection all linked to a control system. Achieving manufacturing synergies has proved challenging added to which a number of plant equipment suppliers have gone into administration. The growth of the biogas industry in the UK strongly correlates to the level of tariff support and as this has degressed then so has the level of new plant installations. The proposed replacement of the RHI subsidy with the Green Gas Support Scheme is a positive move for the industry although the proposed tariff rates are not significantly different to the outgoing RHI scheme. Therefore it is unlikely that this scheme alone will generate the hoped-for increase in new plant capacity.

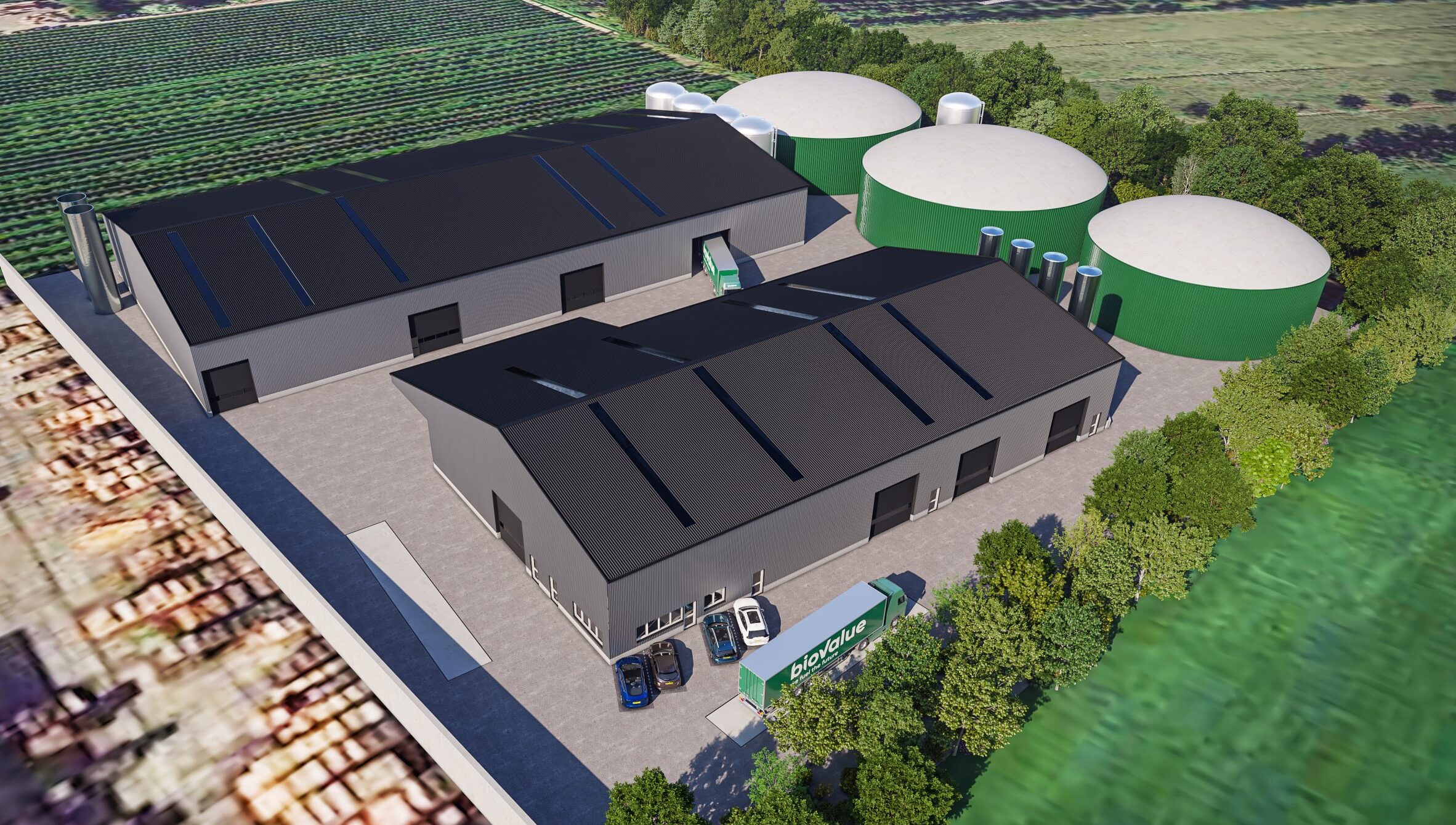

The AD Conundrum

The main constraint on expanding the biogas industry is the availability and price of organic feedstocks. AD plants typically process organic wastes, energy crops and farm residues. Food waste plants have traditionally charged gate fees to process the waste but these have declined as more plants were commissioned. The use of energy crops which were widely used in Germany as a feedstock has been restricted in the UK under sustainability criteria. This, therefore, means that new agricultural AD plants will require a large supply of farm slurries or alternative feedstocks to supplement the energy crops. Sustainability criteria also demand that feedstock is sourced locally so that any new plant needs to be located close to a farm but also close to a large enough gas grid suitable for the injected gas volume proposed. These two factors alone have a significant impact on growing the market. In many ways, AD technology works most sustainably when processing food waste and there are a number of well-established plants processing food waste very efficiently. However future market growth potential is limited by the availability of waste volumes. Therefore most of the new plants being built today are based on the agricultural model of slurries and energy crops.

Value for money is a key issue for any Government tariff support scheme but decarbonisation of the heat network presents significant challenges. Green gas is a natural replacement for natural gas therefore it would be a reasonable policy adoption that any subsidy for green gas should be paid by natural gas suppliers and users. The core assumption on carbon pricing/tax is that the polluter pays, therefore it would be reasonable to let him pay to support the production of green gas. The new RHI tariff replacement is designed to kick start a new phase of green gas expansion and we await to see the actual detail behind the scheme. However, the concern is that without an uplift to the existing tariff levels and a relaxation on the use of energy crops it is unlikely to provide the stimulus to the sector required.

The conundrum is thus, AD as a technology works well and green biogas is an ideal replacement for natural gas as it can utilise the existing distribution infrastructure, however, the industry still requires government tariff support to attract private investment. The key to unlocking the potential for the industry is to find cheaper organic feedstocks with higher biogas yields that comply with a long term sustainable land use strategy.